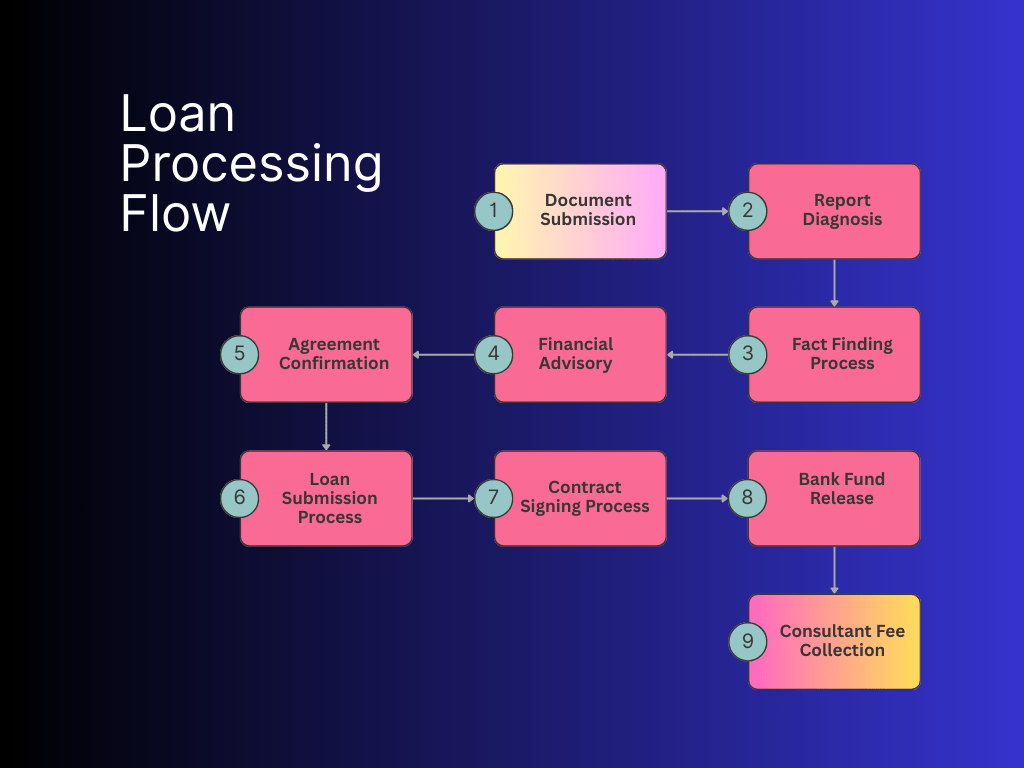

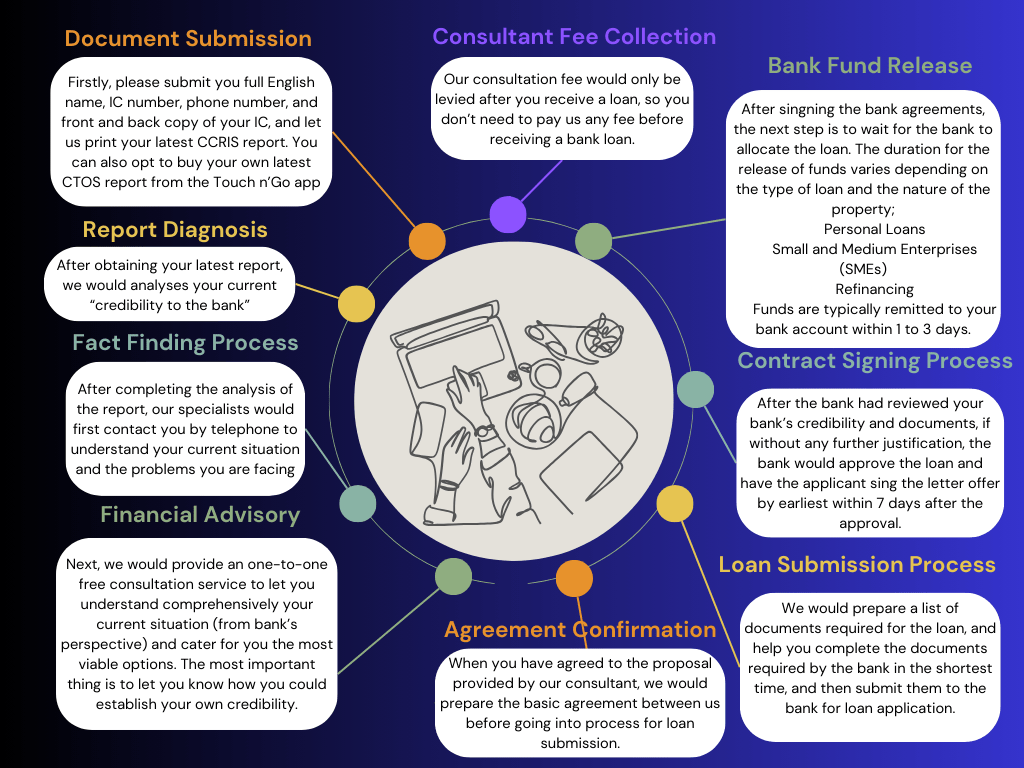

👉 What documents do i need apply for a loan ?

To apply for a loan, you’ll need to prepare several key documents so banks can verify your identity, employments and financial stability such as

🤜 A copy of your identity card ( IC ) or government-issued ID.

🤜 Latest 3-6 month payslips ( for salaried employess) and EPF ( Kumpulan Wang Persaraan ) statements if applicable.

🤜 For self-employed/ business owners – business registration ( SSM ), company financials or tax documents.

🤜 For property loans: documents related to the property ( tittle, strata/ lease information ) and any required valuations.

👉 How long does loan approval take?

🤜 The time to get a loan approved depends on several factors, such as the type of loan you’re applying for. your financial background and how your documnts are.

🤜 For most personal loans, approval and disbursement can happen fairly quickly – usually within a few days to two weeks once all documents are in order.

🤜 More complex cases, such as refinance or property loans, generally take longer as banks need to conduct extra check valuations. Expect at lease one ( 1 ) month for approval and up to three ( 3 ) months or more for the full process.

🤜 More complex cases, such as AKPK or Special Attention Accounts ( SAA ), approvals can take anywhere from 30 to 90 days, depending on how quickly supporting issues are resolved.

🤜 So, while you may see faster outcomes in ideal cases, it’s wise to plan for a 30-90 day window as a realistic expectation

👉 What factors can cause a loan application to be rejected?

🤜 There are several reasons why a bank might reject a loan application, and most are related to how the bank assesses financial risk.

🤜 Common causes include having a high debt-to-income ratio, where your existing financial commitments are too large compared to your income, and a low credit score or poor repayment history reflected in your CTOS or CCRIS records.

🤜 Other frequent issues are incomplete or in accurate documentation, unstable employment history, or being in an industry the bank views as high risk. Sometimes an application is rejected simply because it doesn’t match the bank’s internal criteria or preferred borrower profile.

🤜 Kejora helps you understand these underlying reasons, so you can take the right steps such as improving your credit profile, restructuring your debts, or selecting a more suitable bank before re-applying.

👉 Can i apply for a loan if i’m blacklisted or under AKPK?

🤜 Yes, it’s still possible to apply for a loan if you’re blacklisted or currently under AKPK, but it does require a more strategic approach.

🤜 Banks tend to view such applicants as higher risk, which means approvals are more challenging and may take longer, often around 30 to 90 days, depending on your finance situation. If you have a Special Attention Account ( SAA ) or unresolved debts, some banks may reject your application outright untill those issues re settled.

🤜 This is where Kejora can help: our consultants specialise in loan recovery and restructuring and will guide you to improve your credit, manage your debts, and match you with banks that better fit your profile. With proper planning and professional support, many clients under AKPK or blacklist records have successfully secured financing through the right channels.

👉 Which banks does Kejora work with?

🤜 Kejora works with a wide range of banks in Malaysia, but we don’t submit your application to all of them at once. Each bank has its own loan policies and preferred customer profile, so sending your application everywhere can actually hurt your chances as it may look desperate or raise red flags in the banking system ( similar to asking several friends for money at the same time ).

🤜 Instead, we start by understanding your financial goals and background, then match you with the bank that’s most likely to approve your application with the best possible terms. This strategic approach ensures your profile stands out and gives you a better chance of securing the loan you need.

👉 What is the typical interest rate for bank loans like?

🤜 Interest rates differ from one bank to another and can change depending on the market and your personal profile. Each bank offers different packages based on their own lending policies and current and current trends.

🤜 As general guide, here’the average range of rates you can expect:

↪ Personal Loan: 2.50% – 19.22%

↪ Mortgage Loan: 3.80% – 5.39%

↪ Business Loan: 4.00% – 9.90%

🤜 These figures are only estimates and can vary based on your eligibility, credit score, and the bank’s current base rate (which follows Bank Negara Malaysia’s Overnight Policy Rate).

👉 How long will it take to get my loan once it is approved?

🤜 Loan approval time depends on your financial profile, credit history, and how quickly you provide the required documents.

🤜 As a guide:

↪ Personal loans are usually approved and disbursed about 14 working days

↪ Mortgage or refinance loans may take 3-8 months, depending on the bank’s internal review and document checks

🤜 Be cautious of anyone promising “instant approval” or same-day cash disbursement as legitimate banks don’t process loans that fast.

👉 Do l need to pay any upfront fees?

🤜 No. You don’t need to pay any upfront processing, legal, or stamp duty fees. Kejora does not collect money before your loan is approved

🤜 If anyone claiming to represent Kejora asks for upfront payment, please contact our management immediately. We take such cases seriously and will assist in reporting it to the authorities.

🤜 Thus, Kejora would always first understand your loan objective, subsequently check your financial background and loan eligibility from bank. Then only we would start strategising by submitting your loan application to the bank that best suit your objective and give you the best margin of finance. We ensure a foolproof process in helping you secure your loan.

👉 Why doesn’t Kejora collect upfront fees?

🤜 Many loan scams trick people by asking for payment before approval. To protect our clients, Kejora doesn’t charge any upfront fees.

🤜 We also don’t require prepayment because we understand how stressful loan applications can be, and we don’t want to add to your financial burden.

🤜 You only pay for our consultation after your loan is successfully approved and disbursed by the bank.

👉 Then when does Kejora charge any service fee?

🤜 Kejora only collects its service fee after your loan has been approved and the bank has disbursed the funds to your account. Until your loan disbursement, you won’t be asked to pay a single sen.

👉 How does Kejora make money?

🤜 Kejora earns a service fee only when your loan is successfully approved by the bank. If your application isn’t successful, you pay nothing. This means we’re 100% aligned with your goal we only succeed when you do.

👉 What Kejora consultation fee, and how is calculated?

🤜 Each case is unique, so our consultation fee is calculated based on your loan type and profile.

🤜 Typically, our personal loan consultation fee would fall between 10-30% of the approved loan amount. For example, if you applied for aRM50,000 personal loan with us, the consultation fee would be around RM5,000-RM15,000.

🤜 On the other hand, the consultation fee for a mortgage or refinance loan ranges between 37% of the approved amount. If you applied for a mortgage or refinance loan, the consultation fee would be around RM9,000-RM21,000.

🤜 We’ll always discuss and agree on fees before any process begins.

👉 Can you still help me if I have multiple issues such as past loan rejections, bankruptcy, AKPK, a property facing auction (lelong) or blacklisting?

🤜 Yes. Rejected loans is exactly where Kejora specialises. Many people come to us after being rejected by multiple banks without ever being given a clear explanation. In most cases, applicants are simply told their loan has failed, without proper guidance on why it happened or what they can do next.

🤜 At Kejora, we take a different approach. We believe every rejection has a reason and once the real cause is identified, a proper solution can be planned. Our role is to review your full financial profile, pinpoint the underlying issues, and advise you on the right steps to improve your eligibility before approaching the right banks.

🤜 There is no “magic shortcut” in loan approvals. What we do is help you clean up the root problems, restructure where necessary, and position your application correctly so your chances improve realistically and sustainably.

🤜 Most importantly, don’t feel hopeless if you’re facing these challenges. Many of our clients once felt the same way AND are now back on track with their finances. Kejora is here to guide you every step of the way.